The European Central Bank (ECB) has announced the results of “stress tests”, which assess whether or not banks will fail, or require a taxpayer-funded bailout, if the economy were to turn sour. 130 banks in the eurozone were tested and 25 were found wanting.

The assessment exercise was undertaken by the ECB in advance of assuming its new euro-area banking-supervisor role in early November. The aim is to provide greater transparency in the banking sector, to identify and trigger solutions that will prevent the kind of failings that metastasised in the 2008 financial crisis, and to rebuild confidence in European banks. It is intended to provide a forward-looking view of banks’ shock-absorption capacity.

The good news is that the current 2014 stress testing exercise is tougher and imposes more transparency than previous rounds in 2009, 2010 and 2011. The 25 banks that failed the stress test were found to have had insufficient capital – specifically Common Equity Tier 1 (CET1) capital – to weather a hypothetical but plausible economic storm drawn up by the European Banking Authority (EBA).

No big surprise

These results will not have come as a complete surprise to the participating banks. Early indications of each bank’s standing will have come during the stress test process, which begins with a review of their assets – the Asset Quality Review. Banks have had months to anticipate the eventual stress test outcome and to raise further CET1 capital to make good on any capital required by the stress test.

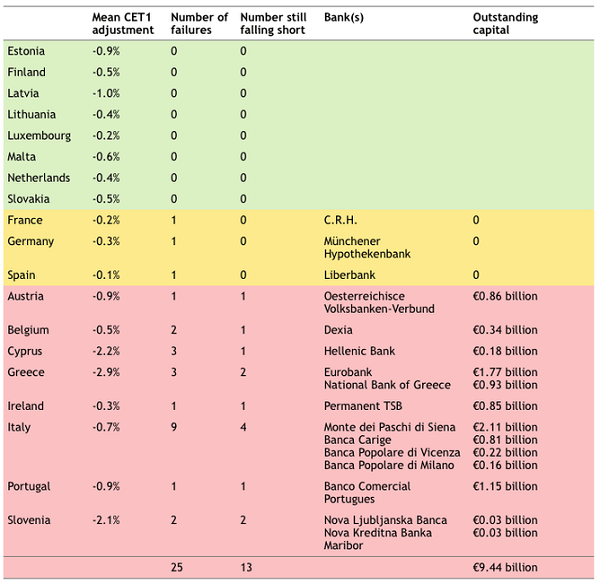

In fact, each of the failing banks in France, Germany and Spain recapitalised in this fashion, so that they no longer have a CET1 capital shortfall. So, it is only 13 banks out of 130 that have really failed the test. These are banks that have not yet fully bolstered their capital buffers to the required levels. They now have two weeks to submit their plans for becoming stress-test compliant within nine months.

The results

The stress test identifies the largest numbers of weak banks in Italy (nine, with four still short of capital), Greece (three, with two still short), and Slovenia (two – both of which are short). In terms of deficiency of capital, Italy and Greece continue to top the list, and though Slovenia has two banks that failed, they are only €0.06 billion short of their capital requirements. (Summary of ECB Stress Test 2014 Results below, author provided)

This relative weakness of Italian and Greek banks is consistent with banking analysts’ prior expectations. But the total capital shortfall identified by the ECB stress test (€25 billion) is at the very low end of what analysts and market participants say is necessary as a buffer in times of financial stress. For instance Goldman Sachs’ September investor survey indicates that the required recapitalisation is of the order of €51 billion.

Landmark process

Given the complexity of the task – riven with competing national interests – and the short, inflexible delivery schedule, these stress test results represent a landmark in institutional and regulatory co-ordination. The process was difficult and even acrimonious early on.

The adverse macroeconomic scenario and associated “normal” baseline were drawn up by the EBA in consultation with the European Systemic Risk Board (ESRB), the ECB and the respective national Competent Authorities. The implications of these findings feed into separate analyses of credit risk, market risk, securitisation risk, cost-of-funding and interest income risk, sovereign risk and non-interest income and expenses risk.

Potential threats

The adverse macroeconomic scenario reflects the ESRB’s assessment of the most pertinent threats to stability in the euro-area:

- An increase in global bond yields, driven by a downward price revision of US long-term bonds. This could trigger a sharp repricing of the risk in emerging markets as large amounts of capital flows out of emerging market economies.

- Deterioration of credit quality in less dynamic economies with fragile banking sectors. This could be the result of shocks to aggregate demand or supply, or shocks to real-estate prices.

- Flagging confidence in the credibility of public finance plans due to the failure of policy reforms.

- Potential doubts about the credibility of lender-of-last resort facilities in the event of a bank failure.

A key observation made by both academic and financial-sector commentators is that this scenario does not explicitly address the possibility of deflation in southern Europe. If incorporated into the stress test scenario, this would likely increase the calculated shortfall for many banks.

The impact of the stress tests will be felt over time in more constrained lending and in any possible provisions appearing in future annual accounts. Those banks experiencing difficulties raising the additional required buffer capital may become acquisition targets. Some are known to have received acquisition approaches already.

More importantly, this comprehensive assessment sets a new standard for confidence-building transparency in the Euro area. This is propitious as a stepping stone toward credible regulation and an operational policy to identify and mitigate fragility. However, it bodes less well if the ECB will lack the ability – for whatever reason – to push beyond this newly established benchmark.

- This article was originally published at The Conversation. Read the original article.

What do you think? Share your comments with us below.

Dr Kim Kaivanto teaches on our Economics programmes.

Disclaimer

The opinions expressed by our bloggers and those providing comments are personal, and may not necessarily reflect the opinions of Lancaster University. Responsibility for the accuracy of any of the information contained within blog posts belongs to the blogger.